{kind=link}

Vaccine Market Size & Trends

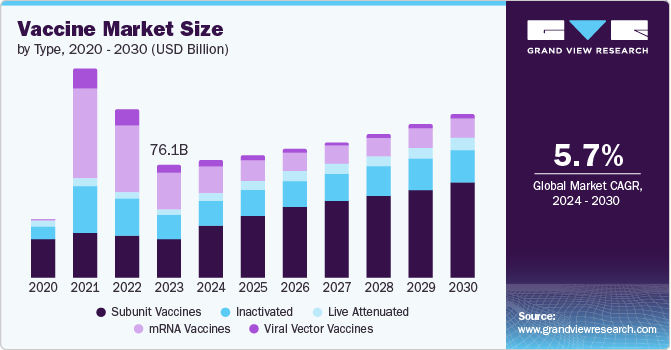

The size of the global vaccine market was estimated to be USD 76.08 billion in 2023 and is anticipated to grow at a CAGR of 5.74% during the period 2024-2030. The vaccine market has been on the rise worldwide, with more vaccines being developed to address diseases that are prevalent in lower-income nations.

In the United States, the market for COVID-19 vaccines shifted to a commercial phase after the exhaustion of the federal government’s bought-up stock. This transition will most likely lead to increased prices, as seen in Moderna’s March 2023 announcement that its price for the COVID-19 vaccine would increase to around USD 110 to USD 130 per dose. The market privatization will also increase competition among producers after the pandemic.

In March 2023, the Serum Institute of India declared its intention to diversify from COVID-19 vaccines by creating new vaccines for dengue and malaria. Company officials, reported that the company has retooled its COVID-19 vaccine production plants to make these new vaccines, which could double its overall production capacity to 4 billion doses a year. This strategic initiative enables Serum Institute to continue producing at high levels and to have quick response capability in the event of future pandemics.

By March 2024, Dr. Reddy’s Laboratories (DRL) will begin promoting and distributing Sanofi’s vaccine brands in India. This partnership includes well-known pediatric and adult vaccines such as Hexaxim, Pentaxim, Tetraxim, Menactra, FluQuadri, Adacel, and Avaxim 80U. These brands collectively generated revenues of approximately USD 51 million as of February 2024. This partnership reinforces DRL’s vaccine portfolio as the second-largest vaccine player in India, with Sanofi still retaining ownership, manufacturing, and importing these vaccines into India.

Regulatory authorities and regional networks have played an important role in building regulatory capacity and fostering coordinated action across nations, resulting in improved access to new vaccines.

The World Health Organization (WHO) has played a pivotal role in doing so, through its prequalification program offering regulatory support and aiding countries in creating effective, stable, and well-integrated regulatory systems. Subsequently, national regulatory authorities across 35 vaccine-manufacturing countries have developed to a maturity level that allows them to effectively regulate development, manufacturing, and release.

Industry Dynamics

Technology trends are also becoming more aligned with enhancing vaccine development processes and availability. There are important advancements in formulations, storage, and delivery methods for increasing effectiveness and efficiency of delivery to various populations.

Furthermore, easy-to-use digital tools are being incorporated to track vaccination coverage and manage supply chain issues. This technology is driving a more effective and expansive impact in disease control against pneumonia and other diseases. These trends are likely to continue influencing the market, promoting improved health outcomes worldwide.

Type Insights

The mRNA category led the vaccine market with a 32.32% share in 2023. In the area Pfizer/BioNTech and Moderna have become well-known with their mRNA COVID-19 vaccines. These vaccines have a significant advantage over traditional vaccines, including the potential to rapidly re-optimize antigen design and combine sequences from several variants to meet new mutations within the virus genome.

This flexibility has been a driving factor in their market leadership. The success of mRNA-based COVID-19 vaccines also led to the development of mRNA platforms for the prevention of other infectious diseases like flu and RSV.

Route Of Administration

Parenteral administration is most preferred for vaccine administration and thus the segment also ruled the vaccine market with a market share of 97.01% in 2023. Parenteral administration, i.e., injection into the body, is most preferred due to higher absorption, better efficacy, and lower risk of contaminations and degradation. Now most vaccines available in the market are intramuscular or subcutaneous, which also helps the segment become the market leader.

Disease Indication Insights

The segment of viral diseases is also classified under Hepatitis, Influenza, HPV, MMR, Rotavirus, Herpes Zoster, COVID-19 and others. This segment dominated the market with a market share of 63.79% in 2023 primarily because of COVID-19 vaccines. Increasing incidence of viral diseases, growing awareness towards vaccination benefits, and initiatives of government towards implementing immunization programs drive the market. The market is competitive and is led by giant companies like Pfizer, GSK, AstraZeneca and Serum Institute among others.

Age Group Insights

Adult contributed 57.25% to the market of vaccines in 2023. Adult vaccination, such as those for COVID-19, constituted 75% in volume in the whole world, while pediatric vaccines were responsible for around 20%. Compared to pre-Covid, volumes of adult vaccines had nine-fold growth largely as a result of COVID-19 vaccination. Additionally, volumes of non-COVID-19 adult vaccines rose by 15% due to extensive application of seasonal influenza vaccination among high-income countries (HICs).

Distribution Channel Insights

Government suppliers accounted for 59.90% of the vaccine market in 2023. Unlike other pharmaceutical products, vaccines are largely funded by public funds in the form of government and pooled procurement schemes with little role for private sector procurement. Concentrated demand can help plan necessary supply investments. Predictability of demand is still a strong driver influencing vaccination access.

Hospital & retail pharmacies supply channel was the estimated quickest growing vaccine distribution channel. In addition, the role of pharmacies as a vaccine supply source in most developed countries has increased further. Pharmacies offer convenient public vaccination access and contribute to a rise in vaccination rates. Moreover, opening up the private market for COVID vaccines in 2023 in the U.S. will further aid the growth in the market.

Regional Insights

North America vaccines market will grow at a fastest CAGR of 8.42% during the forecast period. Government policies to increase immunization and increased awareness after the pandemic fuel adoption. For example, the Hepatitis B Foundation actively endorses the revised adult hepatitis B vaccine recommendations issued by the U.S. Centers for Disease Control and Prevention (CDC).

The Foundation is proactively working with a panel of experts to make these guidelines effectively implemented in order to improve vaccination coverage against this lethal virus for millions of U.S. adults. In the United States, chronic hepatitis B infects an estimated 2.4 million people, killing thousands each year from the disease. If untreated, chronic hepatitis B has a high 25% to 40% lifetime risk of leading to the frequently fatal liver cancer condition.

U.S. Vaccines Market Trends

The U.S. vaccines market held the largest revenue share of the global vaccine market in 2023. Technological advancements at a fast rate, recent U.S. FDA approvals for influenza vaccines, and high competition among firms are poised to drive the market during the forecast period.

For example, in June 2022, CSL Seqirus reported the completion of a USD 156 million expansion at its U.S. manufacturing facility. The expansion is anticipated to enable the formulation of its cell-based influenza vaccines in prefilled syringes.

Further, in October 2021, Seqirus reported U.S. FDA approval of its quadrivalent influenza vaccine FLUCELVAX QUADRIVALENT. This recently licensed vaccine boasts a broader age indication for infants as young as 6 months of age. Additionally, this product is the first and only cell-based influenza vaccine licensed in the U.S.